Table of Content

Simply enter loan amount, interest rate and loan tenure to get all details. For advanced users, use prepayment and taxes options to simplify the complex EMI calculations on home loan. Bajaj Housing Finance provides a hassle-free way for individuals to calculate and view an amortization table for a Home Loan. Simply navigate to our Home Loan EMI Calculator and enter housing loan details, such as loan amount, tenor and rate of interest, to compute such data.

Although it can technically be considered amortizing, this is usually referred to as the depreciation expense of an asset amortized over its expected lifetime. For more information about or to do calculations involving depreciation, please visit the Depreciation Calculator. We have a network of + branches, sales teams and processing centers across the country to cater to the housing loan requirements of individual customers. Please click here to locate us and contact us for your home loan requirements. Please locate us and contact us for your home loan requirements.

EMI CHART

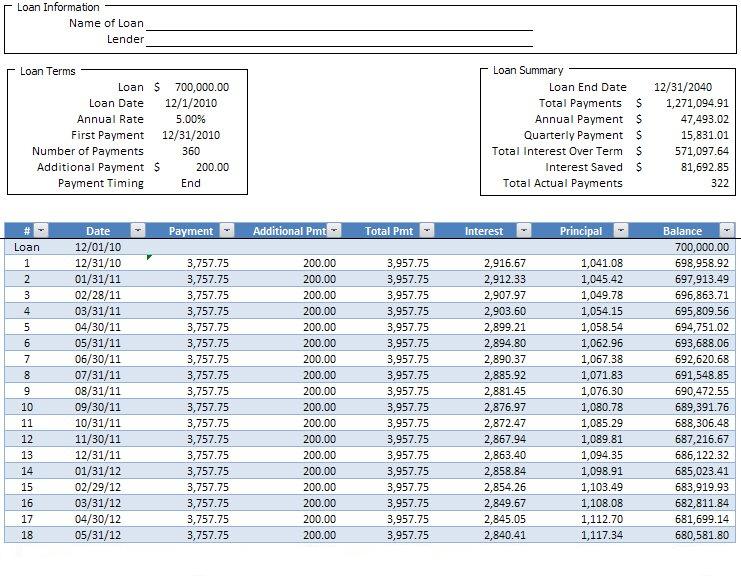

In the first month, the interest component is high while the principal is lower. With the reduced outstanding every month, the interest component goes down while the principal goes up. To calculate the amortization schedule and determine the loan repayment schedule, fill in the boxes given below and click 'Show Amortization Table'.

The number you have suggested gets attributed with regard to the percentage value, thus you don’t need to enter the % marker. Once you have made your decision on a bank to apply for your home loan, the bank will verify the documents you have submitted. Generally, the documents required by the bank are – your name, complete valid address, age, income verification, and the selected property. Every loan you take comes with their own eligibility factors that, as an applicant, you have to fulfill. Apart from that, you should also know the amount you can comfortably pay as EMI every month.

Things to know before you foreclose your Home Loan

The use of any information set out is entirely at the User's own risk. ICICI Bank does not undertake any liability or responsibility to update any data. No claim (whether in contract, tort or otherwise) shall arise out of or in connection with the services against ICICI Bank. The second is used in the context of business accounting and is the act of spreading the cost of an expensive and long-lived item over many periods. By clicking "Proceed" button, you will be redirected from SBI website to the resources located on servers maintained and operated by third parties. SBI doesn't take any responsibility for the images, pictures, plan, layout, size, cost, materials or any other contents in the said site.

The borrower gets several incentives like personal accident insurance and furnishing loan at the home loan interest rate. Other securities are obtained if the mortgage is not possible at loan disbursement. Bank of India Home Loan EMI Calculator is best used fruitfully to compare similar EMIs offered by different leading banks. Comparison is ideally made by trying out varying inputs in contrasting permutations and combinations for an accurate appraisal. SBI Frequently asked questions , has listed questions and answers, all supposed to be commonly asked in context of Home Loans.

MaxGain Home Loan Calculator

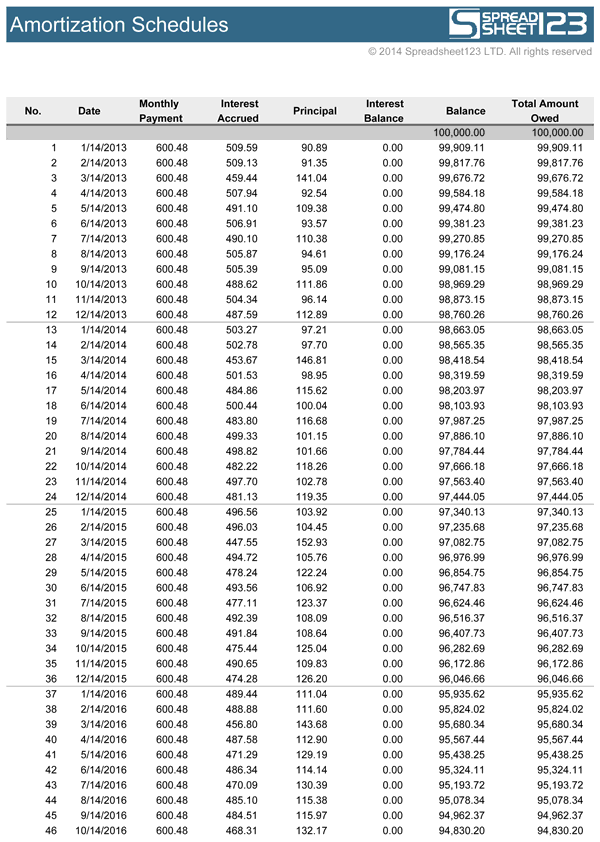

An amortization schedule for a Home Loan is similar to that of other term loans. The only major difference is that since home loans have a significant repayment tenor, this repayment table tends to be longer and more elaborate. The calculation performed by calculator is based on the information you provided and is for illustrative purposes only. This calculation reflects amounts in Indian Rupee and estimated monthly payments do not include any processing or other possible fees.

Schedules prepared by banks/lenders will also show tax and insurance payments if made by the lender. In other words, a schedule which shows repayment broken down by interest and amortization and the loan balance. Loan Amortization is the gradual repayment of a debt over a period of time. In order to amortize a loan, your payments must be large enough to pay not only the interest that has accrued but also to the principal. Your home loan EMI is the monthly payment that you make to repay the home loan as per the amortisation schedule.

After every EMI credit, the outstanding loan balance helps the applicant chart prepayment to impact the home loan financials. The sample Amortization Table below with the identical inputs for the EMI illustration is indicative of its various utilities. The home loan is repaid over the chosen tenure in installments for the entire cost of the loan calculated with the applicable interest rate and other admissible charges.

According to IRS guidelines, initial startup costs must be amortized. Click on the print/download button to Download your home loan EMI calculation and home loan amortization schedule. HDFC also offers a facility of a pre-approved home loan even before you have identified your dream home. A pre-approved home loan is an in-principal approval for a loan given on the basis of your income, creditworthiness and financial position. It includes repayment of the principal amount and payment of the interest on the outstanding amount of your home loan. The principal component of each payment will be increasing during the life of the loan.

This calculator also performs the calculations at a lightning speed, so that you have time to make other important decisions of your life. Transferring your outstanding home loan availed from another Bank / Financial Institution to HDFC is known as a balance transfer loan. An online EMI calculator is easily accessible online from anywhere.

Bank of India applies only the floating interest rate on their home loan products daily, reducing balance at monthly rests. The interest burden is reduced to liquidate the home loan before the tenure is over when additional funds are available. As it is self-explanatory by its name, the interest charges on your home loan subjected to current lending rates of the bank.

No comments:

Post a Comment